Hi, we're looking for banks, PAG-IBIG, lending companies, etc that offers the lowest annual interest rates and charges on housing loan.

Please feel free to post if you know any of the ff:

- loan amount bracket and corresponding term

- interest rate per annum (diminishing or fix)

- charges (service charge, etc), fees and penalty (late payment)

- requirements (will be using employed status)

- without collateral

We're planning to have it spot cash with 0% staggard payment sa in-house financing unta pero Bank Financing mn ila nabutang. Naka-realize sad mi nga it's better to loan nlng ky we can still use the money on other things and di siya bug-at if longer payment term.

When needed: approx. March to April 2013 pa.

Mods, if ever with duplicate na. Please delete nlng this post. Thank you.

UPDATE: Housing Loan

1. Banks

a. Interest Rate

- ranges from 5 to 12 % p.a.

- so far, diminishing

b. Bank charges

- comprise appraisal fee doc stamp, etc

- may reach upto 30k+ for 1M Principal Loan

c. Years of fixing

- Yearly, 2 years, 3 yrs., 5 yrs., 10 years or full term fixed rate.

- The longer the duration of years of fixing, the higher the interest rate.

(You can decide on the number of years of fixing according to your capacity to pay and to how you view the market trend.)

d. MRI (Mortgaged Redemption Insurance)/ CLI (Credit Life Insurance) & Fire Insurance

- pwede attach sa ila and to your amortization or you get it separately

- payment may be staggard or annually.

- Yearly renewable and is dependent to the outstanding principal amount

Full Payment of Loan:

a. Notarial Fee

b. Letter of Release/ Cancellation of Mortgaged Annotation

c. Acceleration Fee (may not be applicable to some banks)

Cancellation of Mortgaged Annotation:

- To be processed by the client's end.

Where: Registry of Deeds

Maceda Law: "Rights of a Defaulting Buyer under RA 6552"

Right to update payments without additional interest or in the alternative a refund of cash surrender value.

There are two categories of buyers accorded protection under this law:

1. a buyer with at least 2 years of installments under Section 3 RA 6552, and 2. a buyer with less than 2 years of installments under Section 4 RA 6552

Buyer with at least two (2) years of installment Section 3 RA 6552 If the buyer in this category defaults in the payment of his succeeding installments, he is entitled to the following rights: 1. to pay without additional interest the unpaid installments due within the total grace period earned by him. Said grace period is equal to one (1) month for every year of installment payments he has made. Here the buyer has at least two (2) months grace period for he should have paid at least two (2) years of installments to avail of the rights under this section.

This right can be exercised by the buyer only once in every five years of the life of the contract. 2. to be refunded of the cash surrender value of his payments equal to 50% of his total payments if the contract is cancelled. But if he has paid five years or more, he is entitled to an increase of 5% every year and so on but the cash surrender value shall not exceed 90% of his total payments.

The actual cancellation of the contract referred to above shall take place only:

1. after 30 days from receipt by the buyer of the notice of cancellation or demand for rescission, AND 2. upon full payment to the buyer of the cash surrender value.

In the computation of the total number of installment payments the following are included: 1. down payment and 2. deposit or option money

Section 3 of RA 6552 provides, thus:

SECTION 3. In all transactions or contracts, involving the sale or financing of real estate on installment payments, including residential condominium apartments where the buyer has paid at least two years of installments, the buyer is entitled to the following rights in case he defaults in the payment of succeeding installments:

(a) To pay, without additional interest, the unpaid installments due within the total grace period earned by him, which is hereby fixed at the rate of one month grace period for every one year of installment payments made; provided, That this right shall be exercised by the buyer only once in every five years of the life of the contract and its extensions, if any.

(b) if the contract is cancelled, the seller shall refund to the buyer the cash surrender value of the payments on the property equivalent to fifty per cent of the total payments made and, after five years of installments, an additional five per cent every year but not to exceed ninety per cent of the total payments made; provided, That the actual cancellation of the contract shall take place after thirty days from receipt by the buyer of the notice of cancellation or demand for rescission of the contract by a notarial act and upon full payment of the cash surrender value to the buyer.

Down payments, deposits or options on the contract shall be included in the computation of the total number of installment payments made.

Buyer with less than 2 years of installments Section 4 RA 6552 If he has paid less than two (2) years of installments, he still has the right to pay within a grace period of not less than sixty (60) days from the date the installment became due.

If the buyer fails to pay the installment due at the expiration of the grace period, i.e. 60 days, the seller may cancel the contract after 30 days from receipt by the buyer of the notice of cancellation or demand for rescission of the contract by a notarial act.

Here the buyer is not entitled to any refund.

Section 4 of RA 6552 provides, thus:

SECTION 4. In case where less than two years of installments were paid the seller shall give the buyer a grace period of not less than sixty days from the date the installment become due. If the buyer fails to pay the installments due at the expiration of the grace period, the seller may cancel the contract after thirty days from receipt by the buyer of the notice of cancellation or the demand for rescission of the contract by a notarial act.

Right to Assign/Reinstate Contract

The buyer has a right to sell or assign his rights over the lot or unit to another person or reinstate the contract by updating the account provided this is done during the grace period and before actual cancellation of the contract.

Section 5 of RA 6552 states:

SECTION 5. Under Sections 3 and 4, the buyer shall have the right to sell his rights or assign the same to another person or to reinstate the contract by upgrading the account during the grace period and before actual cancellation of the contract. The deed of sale or assignment shall be done by notarial act.

Right to Advance Payment without Interest and Annotation of Full Payment in the Title Subject of the Sale

The buyer has the right to pay in advance any installments or the full unpaid balance without interest any time and have such full payment annotated in the title.

Section 6 of RA 6552 states:

SECTION 6. The buyer shall have the right to pay in advance any installments or the full unpaid balance of the purchase price any time without interest and to have such full payment of the purchase price annotated in the certificate of title covering the property.

Transfer of Title through Deed of Sale (Non-Corporation):

1. Secure Checklist form at Registry of Deeds

Documents Needed:

1. Deed of Sale

2. BIR CAR/ Tax Clearance Certificate

3. Documentary Stamp Tax Receipt

4. Owner's and all issued Co-Owner's Duplicate Certificates

5. Realty Tax Clearance

6. Tax Declaration (Certified Copy) at Assessor's Office

7. Transfer Tax Receipt at Land Tax Office

Source: Registry of Deeds

Last edited by cebu.opportunities; 01-27-2016 at 10:57 AM.

Advance Payment:

- will be acknowledged only per anniversary date of loan

- at least 6 months of amortization or (current month amortization plus 5 months advance payment)

Note: Both Metrobank and PS Bank will not easily give you the list of loan requirements not unless the property is affiliated and you are more likely legible for their housing loan.

Last edited by cebu.opportunities; 03-06-2013 at 07:22 PM.

Interest Rates (p.a.) as of January 04, 2013: House and Lot

(source: seminar)

1 year - 7.50%

2 to 3 years - 8.75%

4 to 5 years - 9%

6 to 10 years - 10%

11 to 15 years - 11%

16 to 20 years - 11.5%

Interest Rates (p.a.) as of January 23, 2013: Condo

(source: BPI personnel)

1 year - 6%

2 to 3 years - 7.75%

4 to 5 years - 8%

10 years - 10%

Interest rates

- can be fixed on a given term and be fluctuating thereafter; can be fixed all throughout the loan term

- diminishing interests

Payment

- no preterm payment penalties

- no advance payment charges

- interest is fix for the month's loan balance and the add-on payment to the amortization will be deducted to the principal amount

Fees

- Appraisal Fee of P3.5K (as of Jan. 2013); Appraisal fee will be waived if property is of affiliated developer.

- Mortgage Registration fees

- Mortgage redemption insurance premium

- Fire/Lightning/ Typhoon/ Earthquake/ Flood (Acts of Nature) insurance premium

- Notarial Fee

- Life insurance (not in the list but spoken by the Loan Banking Relationship Manager)

- if with existing life insurance, no need to secure another life insurance unless,

- your "pre-granted" loan amount is higher than the amount insured;

- Amount insured should equate or at least be with the similar amount but to be less than the loan

- In cases that the amount insured is lesser than the loan amount, secure another life insurance plan to suffice the principal amount.

- If the amount insured in a single Life insurance Policy is way higher than the loan amount, a portion of it will just be used to pay the bank in case of the borrower's death.

bye the way wala ko kagets sa pama age aning housing loan...pwede can someone can explain mi regarding this maater?? until now naglibog pa gihapon ko ani......

BPI or BPI Family Housing Loan

- 5 working days of credit decision

Steps: Condo

A. Credit Assessment, Appraisal and Evaluation

1. Secure the term sheet from the developer which contains the ff:

- Unit Number

- Appraisal Value or Total Contract Price

- Your name

- Term, Installments and (amount paid-- may not be included)

2. Basic Application

- Duly accomplished application form

3. Income document (depending on income source)

- If ITR (Income Tax Return) or income shows incapacity to pay, co-borrower is needed.

- Amortization is based on 40% of your monthly income.

4. Collateral Documents

5. Fees

Checklist of Requirements

For all applicants:

- Duly accomplished application form

- Marriage Contract (if married)

- 2 Government Issued ID's

- Latest Residence Certificate (Cedula)

- 1pc. 2x2 picture

If LOCALLY employed:

- Certificate of employment (COE) indicating salary, position and length of service

- Latest Income Tax Return (ITR)

- 3 months payslips/paystubs

- 3 months bank statement

If OFW:

- Certificate of Employment (COE) with email address of supervisor or HR

- Latest Contract and Certificate of Employment from agency (for seaman)

- Original payslips for the last 3 months

- Proof of remittance for the last 3 months

If Self-Employed:

- Articles of Incorporation/By-laws/SEC Registration

- DTI Registration

- Mayor's Permit or Business Permit

- Latest Income Tax Return

- Bank statements for the past 3 months

- List of Trade references (at least 3 names w/ telephone nos. of major suppliers/customers)

If Practicing Doctor:

- Clinic addresses and schedules

- Bank statements for the past 3-6 months

- Latest Income Tax Return (ITR)

If from Commission:

- Vouchers/ Bank Statements (for the last 6 months reflecting commission income)

If Pensioners:

- Pension Papers

- Proof Pension - Bank Statements or Receipts

If from Rental of Properties:

- Rebtal/ Lease contracts (indicating name of tenants and rental amounts w/ complete addresses of properties being rented)

- Photocopy of Title (TCT/CCT)

Additional Requirements:

- Citizenship Retention Certificate or Oath of Allegiance (for dual Citizens)

- Transferees Affidavit (for naturalized foreign citizens)

Collateral Documents:

- Photocopy of Individual TCT/CCT (Owner's Duplicate Copy; 2 copies)

- Photocopy of Tax declaration on lot and building

- Photocopy of Tax Receipt/Tax clearance

- Lot Plan / Vicinity Map

- Non-refundable Appraisal Fee of P3,500.00

Collateral Documents (Construction):

- Photocopy of Individual TCT/CCT (2 copies)

- Photocopy of Tax declaration on lot and building

- Photocopy of Tax Receipt/ Tax Clearance

- Lot Plan / Vicinity Map

- Bill of Materials

- Building Plan

- Building Permit from OBO

- Non-refundable Appraisal Fee of P3,500.00

- Statement of Account from developer / Term Sheet (if collateral is accredited)

Last edited by cebu.opportunities; 02-12-2013 at 07:30 PM.

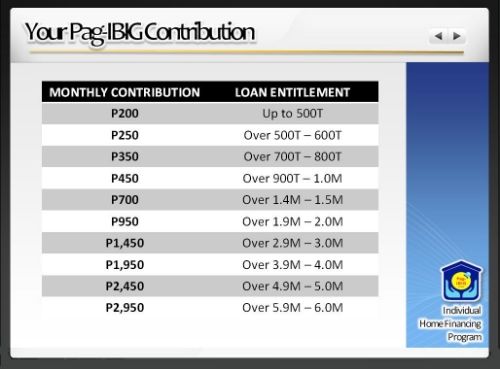

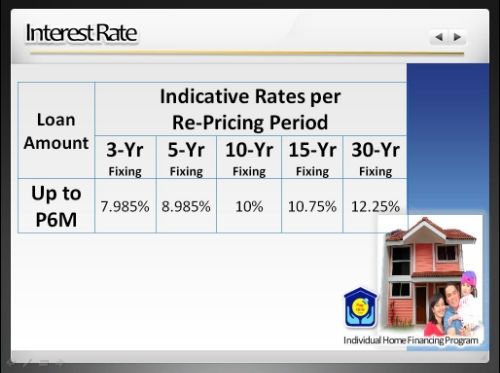

Individual Home Financing Program

HDMF Circular 310

Enhanced Housing Loan Program: year 2013

- increased Maximum Loan to PhP 6M

- Enhanced Portfolio Categorization

I. Affordable Housing Loan

II. Regular Housing Loan

Who are eligible?

1. All Active Pag-IBIG members with:

- at least 24 months contributions

- not more than 65 years old at the date of loan application, insurable and is nor more than 70 years old at the date of loan maturity

- legal capacity to acquire and encumber real property

- No outstanding Pag-IBIG housing loan

- No Pag-IBIG housing loan foreclosed, cancelled, bought back, or voluntarily surrendered

- If with existing Pag-IBIG Multi Purpose Loan (MPL), payments should be updated upon Housing Loan application

Loan Purpose:

- Purchase of residential lot

- Purchase of house and lot, townhouse or condominium unit (old, new or acquired asset)

- Construction or completion of residential unit

Interest Rate: Affordable Housing

Loan Amount- Loans up to 400K

Interest- 4.5%

Cluster 1 (NCR)- GMI up to 15k

Cluster 2 (REGIONS)- GMI up to 12k

Loan Amount- Loans up to 750K

Interest- 6.5%

Cluster 1 (NCR) - GMI up to 17.5k

Cluster 2 (REGIONS) - GMI up to 14K

Regular Housing Loan

Loan Purpose:

- Purchase of residential lot or adjoining lots (max 1,000 sq.m.; min 28 sq.m.)

- Purchase of house & lot, townhouse or condominium unit (adjoining units)

- Construction of house

- Improvement of house

- Refinancing of an existing loan

Combined Loan Purposes:

- Lot purchase with house construction

- Purchase of residential unit with home improvement

- Refinancing with home improvement or house construction

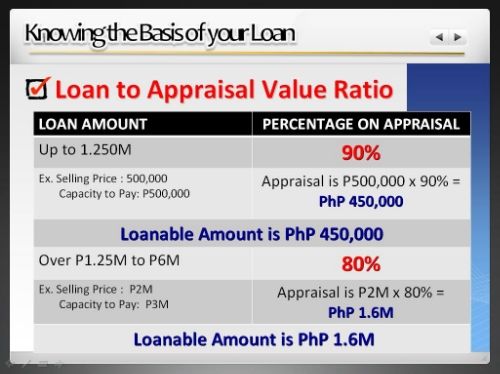

Shall be based on the lowest of the following:

1. Actual Need

a. PRU: Selling Price

b. House Construction: Total Construction Cost

c. Refinancing: Outstanding Balance

2. Capacity to Pay

a. 35% of your Gross Monthly Income, for loans up to P1,250,000

b. 30% of your Gross Monthly Income, for loans over P1,250,000

c. Tacking Provision: Maximum of three (3) qualified Pag-IBIG members

3. Loan-to-Appraisal Value Ratio

Loan Term:

- Maximum of up to 30 Years provided that:

----> Principal borrower's age shall not exceed 70 years old at date of loan maturity.

Last edited by cebu.opportunities; 02-12-2013 at 12:46 PM.

Housing Loan

Housing Loan

Originally Posted by cebu.opportunities

Originally Posted by cebu.opportunities

Reply With Quote

Reply With Quote Posting Permissions

Posting Permissions